The 1 January 2026 renewal season is unfolding as an orderly and strongly buyer‑tilted market, underpinned by record reinsurance capital and growing competitive pressure to deploy it. Cedents are using this window to seek meaningful rate relief, broader coverage terms and fewer exclusions. Reinsurers, on the other hand, are working to keep the pricing and underwriting discipline that has been evident over the last three years.

Reinsurance capital has grown significantly, driving market dynamics

Guy Carpenter estimates that global reinsurance capital reached a new high of about $660 billion by 30 June 2025, driven largely by retained and redeployed earnings across both traditional and alternative markets. Aon and others characterise the 2026 season as starting from a position of “favourable reinsurance market dynamics”. Similar capital numbers were reported by Aon Re ($735 billion) and Gallagher Re ($710 billion).

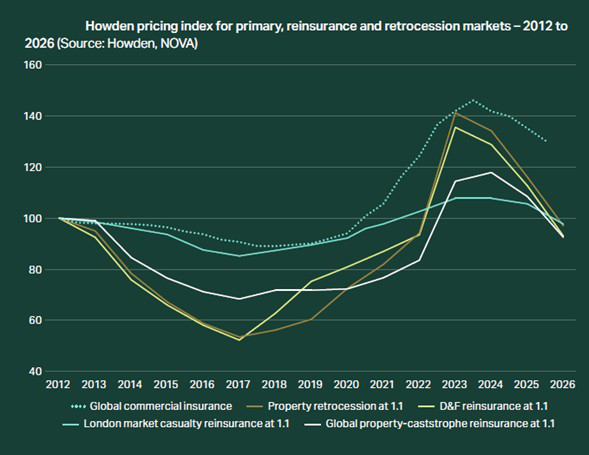

This capital led to significant rate reductions for reinsurance (see graph below). Buyer preferences have generally focused more on reducing cost via the rate reductions rather than structural changes to increase cover. Indeed, pricing has been the dominant story: strong 2025 returns and subdued demand driving a general rate reduction trend. Rates across most reinsurance lines have fallen sharply, as illustrated by Howden Re’s analysis.

With demand for reinsurance cover not keeping pace with available capital (which grew by 8.7% in 2025), rates have continued to soften. The reinsurance capital available has grown significantly, with Guy Carpenter estimating $660bn in capital (noting that Aon reports a higher estimate of $735bn).

Property catastrophe and retrocession

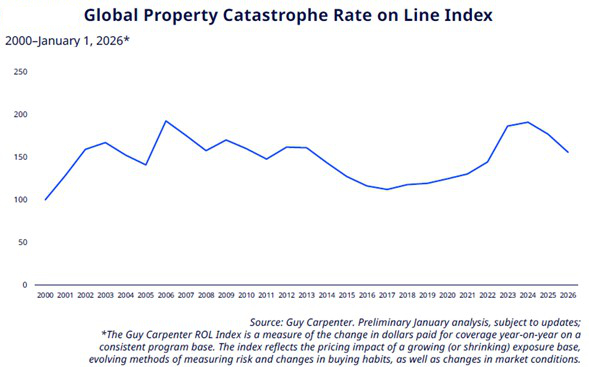

Property catastrophe is at the centre of the softening narrative for 1/1 2026. Moody’s Ratings expects property cat reinsurance pricing to decline by around 15% over the coming year, with variations by region and peril, but an overall buyers’ market tone. This is despite catastrophe losses that exceeded $100bn for the sixth year in succession even with limited hurricane losses during the period.

Guy Carpenter paints a picture of continued high attachment points for property reinsurers which, along with plentiful capacity, are driving competitive pricing conditions. Their Rate- on- Line index for Property Catastrophe risks is showing the market peaked in 2024 and is now returning closer to the long-term average. A key question is whether the rate reductions continue or stabilise at their current levels.

Amwins’ 2026 outlook points to double‑digit cost reductions on many treaty placements, particularly at higher excess points where cat exposure is more remote and competition from alternative capital is most intense. Underwriting standards have “loosened modestly”, with reinsurers more flexible on terms and line sizes.

Our own analysis describes the phase shift as a move from three years of hard market conditions to a “buyer’s market”, albeit one still expected to deliver very profitable outcomes for reinsurers amid moderate 2025 catastrophe losses.

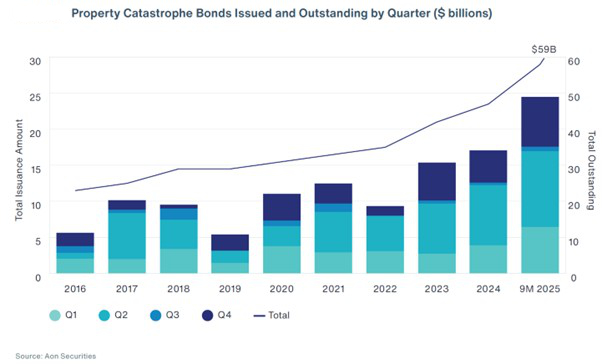

Retrocession and Insurance Linked Securities (ILS) are amplifying this reduction. Analysts note that retro rates for 2026 are expected to fall even more than direct treaty, while ILS investors are widely anticipated to roll profitable 2025 earnings into fresh capacity, further strengthening supply at the top of programmes. This dynamic allows many cedents to top up limit, tidy tower structures and, in some cases, explore modest reductions in retentions without materially compromising reinsurer returns.

The growth in alternative capital for reinsurers (e.g. ILS, catastrophe bonds and sidecars) . demonstrates how the market continues to innovate on the capital side. While this innovation has been generally positive, the growth in this capital has been substantial over the last year (see graph below).

As reinsurers increase their use of alternative capital, questions remain about the sustainability of this new capital approach. As a fundraising strategy, it works well while there are no catastrophes, but if a catastrophe hits a major town centre resulting in significant losses, there is a potential for capital to be harder to obtain if investors pull out of the ILS market.

Updates on Property, casualty and multi‑line treaties

Outside peak cat, Hannover Re expected a “continued attractive market environment” at 1 January, with overall property‑and‑casualty treaty prices stable to slightly lower and terms, conditions and retentions on an “unchanged good level”. The reinsurer plans to make more capacity available at 1/1, but explicitly ties this to risk‑adequate pricing, signalling that structural give‑backs will be controlled even as headline rates trend down.

Howden reports that most specialty casualty lines continued to perform well at 1/1, improving outcomes for cedents. Greater loss clarity from ongoing geopolitical events meant less uncertainty, enabling buyers to benefit from broadly favourable market conditions.

Supporting this, Gallagher Re reports a growing appetite from alternative capital to access to long-tail space.

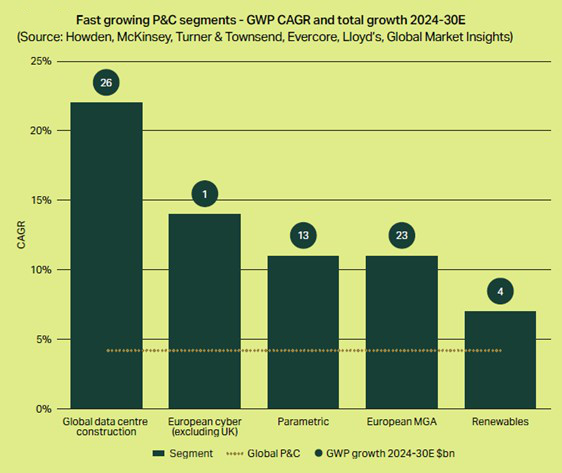

Certain segments of the P&C market are forecast to grow at a faster rate, based on data from Howden Re, with global data centres expected to grow the fastest as demand for AI services increase.

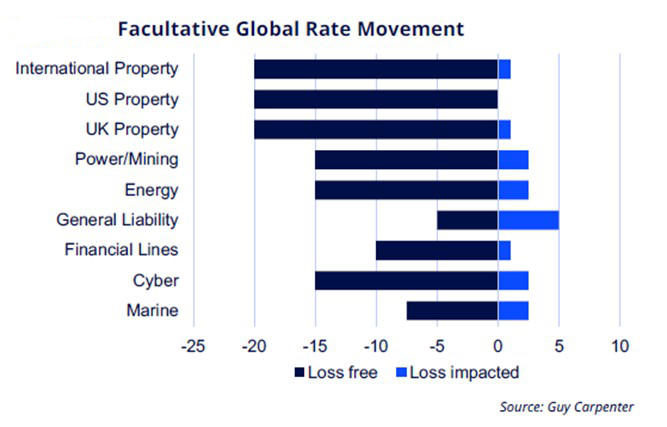

Treaties with less claims were rewarded with bigger rate reductions

For facultative cover, rate changes were impacted by whether losses had occurred or not, with far steeper reduction for treaties with no losses:

John Welch of Aspen notes that casualty treaty renewals have “been fairly disciplined”, with cedents pushing for rate reductions and some treaty concessions but reinsurers keen to avoid repeating past cycle mistakes. Unsurprisingly, reinsurers are most willing to offer improved terms on programmes that demonstrate sound pricing and a clean claims history.

Strategic Implications for key players

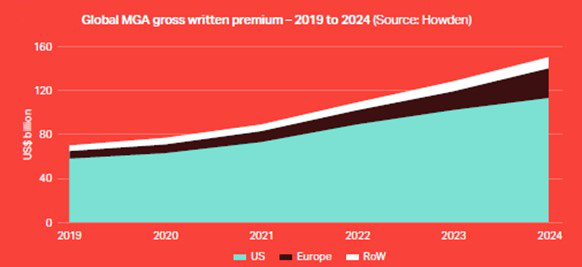

- The MGA market is the big winner

The growth in the MGA market (see graph below) demonstrates the primary insurance market’s vitality. When reinsurance rates soften and capacity expands, MGAs benefit and potentially reduce the global insurance gap due to their rapid innovation, speed and flexibility of cover.

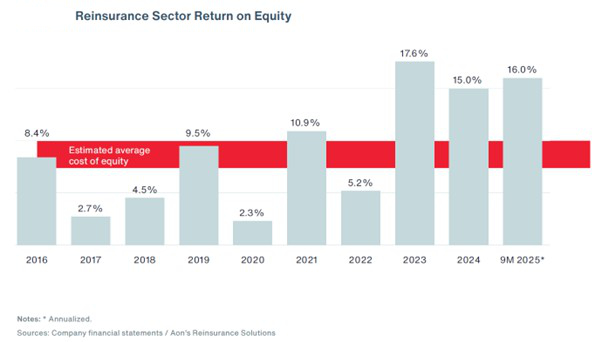

- Reinsurers remain highly profitable, but with some headwinds in future

The strongest theme from the 1/1 renewals is that reinsurance transactions favour buyers, . however, 2026 is still expected to be one of the most profitable years for reinsurers in recent history. KBW reports executives describing 2026 as potentially the “fifth‑best year” ever for catastrophe reinsurance, even after expected rate cuts thanks to increased attachment points, improved portfolio quality and strong investment income. Aon estimates indicate that reinsurers remain highly profitable, having exceeded their cost of equity over the last 3 years (see graph below).

- Insurers will benefit from cost reductions, and M&A activity will grow

Many insurers have opted to use reinsurance cost reductions to boost profitability rather than materially expand cover. Looking beyond the 2026 renewal, insurers are likely to focus on capital optimisation and portfolio strategy using the expanded menu of reinsurance options to improve returns and manage volatility.

PwC expects insurance M&A activity through 2026 to remain robust, with carriers using both transactions and structured reinsurance, such as sidecars and bespoke capital relief solutions, to manage volatility and free up capital for growth. This reinforces the message that 1/1 2026 is not just a pricing event, but a broader strategic inflection point for how risk, capital and earnings are balanced across the (re)insurance value chain.

Greg is the Head of Insurance Platforms at Optalitix. He manages the analytics team to provide high-quality solutions to insurance companies and banks to provide insight and increase profits. He is a qualified actuary who specialises in Life Insurance, Catastrophe Risk and Investment.