The future of commercial underwriting and how to prepare for it

Why Legacy Pricing Systems Are Holding Insurers Back

Three big insurance industry challenges

The insurance industry is at a turning point and faces three major challenges that will define its future.

The last two years have been incredibly profitable for commercial insurers, but we know this is not sustainable, especially with a softening market. Companies that fail to prepare now will find themselves struggling in the years ahead.

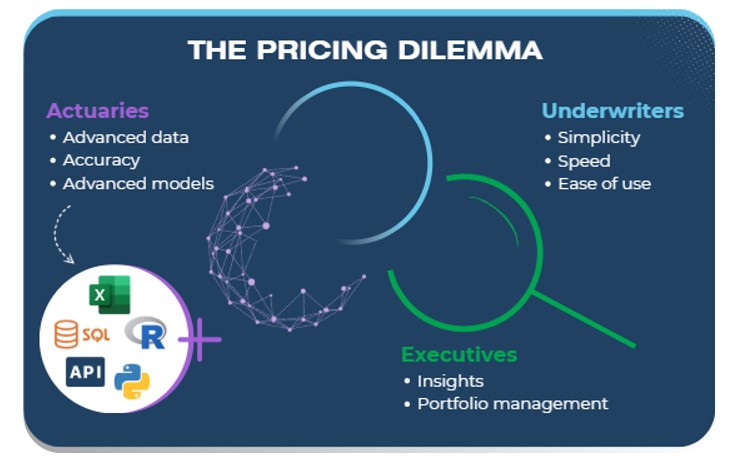

You can’t please everyone all the time…or can you?

Inside every insurance company, three groups influence pricing, and they all have specific needs.

Here’s the challenge: Most pricing systems fail to meet the needs of every stakeholder. They are either too complex for underwriters, too rigid for actuaries, or fail to provide the insights which executives need.

So, how do we fix this?

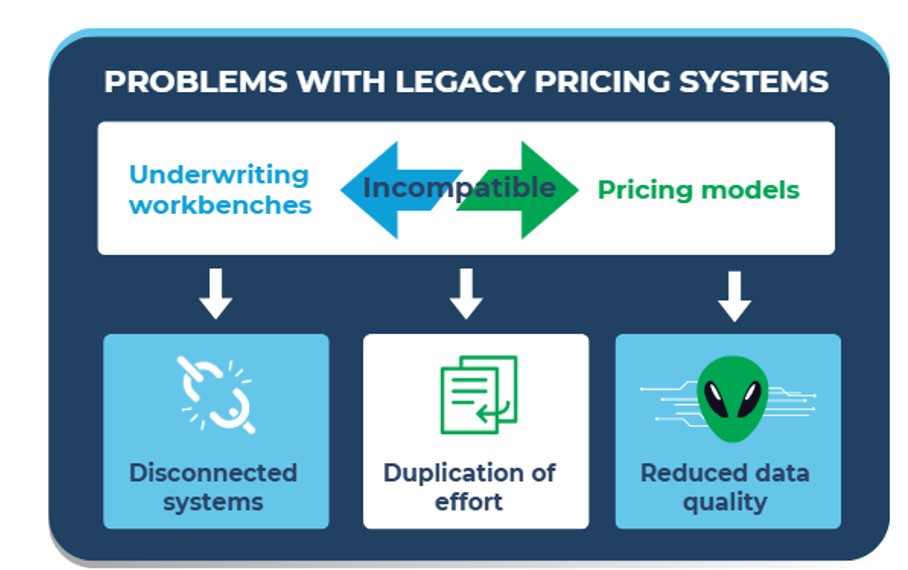

We believe the answer lies in better data which can only be achieved using much tighter system integration, however, legacy pricing systems don’t allow this. There is one common, and major issue; underwriting workbenches and pricing models don’t easily talk to each other.

What are the implications for disconnected pricing systems?

When data outputs don’t flow smoothly, the results include:

· Slowing down of operations

· Impaired decision-making

· Reduced data quality

· A loss of all data for unbound quotes (at least 50%)

· A significant duplication of effort to try and recapture as much pricing data as possible

The reality is that existing systems are not designed for the future. They are slow, expensive, and inefficient.

How do we overcome insurance pricing challenges?

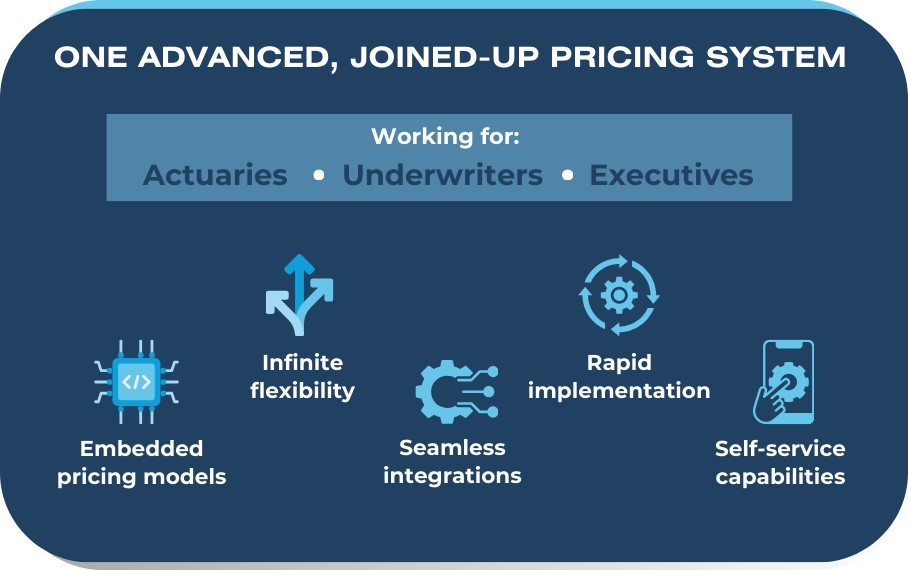

· We need systems that embed pricing models automatically and are flexible enough to accept all the modern actuarial pricing models that are available.

· They need to seamlessly integrate with any existing insurance system to enable good quality data for pricing and risk insights and be quick to go live to prove value.

· They need to be easy to manage by everyone in the business to avoid pricing delays and costly changes.

In short, we need one advanced and joined-up pricing system which can deliver advanced pricing models for actuaries, efficiency for underwriters, and strategic insights for executives.

The future of insurance depends on upgrading pricing systems, NOW

The commercial insurance market is evolving very quickly. The companies that succeed in this incredibly competitive market will be the ones that embrace better pricing, faster technology, and seamless integration.

This is the dream, and what our clients and industry experts tell us they want.

More blogs

Next Generation of AI Described as “Too Dangerous to Release” – Now Released

The Artificial intelligence tool Generative Pre-training Transformer (GPT-3) has gained much attention, but is the technology dangerous?

What part will AI play in the future of commercial insurance pricing?

AI is transforming commercial insurance pricing—are you leveraging its full potential?

The California Wildfires: An industry-defining event

Explore how the California wildfires have become a turning point for the insurance industry. Learn how insurers are adapting through advanced data analytics, risk modelling, and technology.