Why is it that in an environment so dependent on the richness of data, the insurance industry still relies on systems that are built simply to transact? Too many insurers claim to deploy modern, cutting edge technology solutions yet their systems are built to process actions without using the valuable insights from their data that can improve the user experience. By building a system that only gets you from point A to point B, existing insurance systems become processing engines that don’t think.

The guesswork is left to their staff and clients using the system, who often make their own subjective decisions as the system provides no insight, despite the volumes of data available to it.These “dumb” systems are no longer going to cut it with the introduction of new InsurTech companies that focus on the customer experience and bring innovations throughout the insurance process, from sales to administration to claims.The question that needs to be asked at the start of a system design is whether those setting up the processes are equipped with the skills needed to ensure that the system “learns” from the customer journey and is capable of using this to improve the process afterwards. In most cases they are not! As a result, the process is not as efficient and effective as it should be.

When setting up these systems, a clear differentiation needs to be made between the “actions” part of the machine and the “brains”. There is a difference between just “doing” and “processing, learning and improving”. The challenge faced by decision makers tasked with implementing machine learning in their processes is identifying developers who can do two things – build a process and enable it to evolve. There are many smart developers who are great at creating task and goal orientated processes, but developers that create systems to analyse, observe and optimise have a completely different skill set – this requires a fusion of data science and technology.For optimum productivity, data will be fed into a decision engine, models will be developed, algorithms will run, whilst simultaneously feeding back fresh insight into the system, suggesting real time changes to the user experience such as new product offerings, personalised incentives, useful marketing messages and improved claims handling. If systems lack inbuilt data science capabilities, insurers will need to bring in external resources to analyse the data, often using (delayed) offline processes and with higher human costs and biases.

This can compromise the customer journey and reduce efficiency. Sales will be lost due to inappropriate focus, claims will be mismanaged due to routing delays and lapse rates increase due to inefficient retention strategies. The actual cost to the insurer ends up being much higher.Decision makers that recognise the need to design systems to learn will shorten the insight loop by appreciating the value that real time business intelligence can add. They benefit from thinking systems as opposed to processing systems.To be competitive, insurers should be asking how smart their systems are, and whether their processes learn and improve over time. If the answer is no, the guessing game will continue.

What are the four types of artificial intelligence?

Reactive machines, theory of mind, limited memory, and self-awareness are four main types of AI categories to be aware of. Read more about them in this guide.

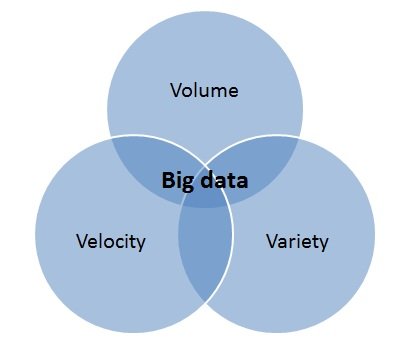

What are the 3 V's of big data?

What are the 3 v’s of big data? Find out more as the data experts at Optalitix explain what they mean by using examples to illustrate each of them.

How to Become a Data Scientist

When pricing a new product, the starting point is almost always Excel. Learn how to create a pricing application from a spreadsheet pricing model here.

Holiday AI Thoughts

The key to selling is to establish a relevant dialogue and understanding with your clients. Find out how AI systems can be used to target the right consumers.

Artificial Intelligence powered insurance is now inevitable!

AI is changing the competitive landscape for insurers by delivering a competitive edge in a number of areas. Read more about AI in insurance.

AI Accessible for all - Ignore at your peril!

As AI continues to develop, businesses of all sizes will need to engage with the technology and embrace the power of machine learning to improve their processes.

The Computable Game

Data analysis with Optalitix—an online underwriting tool offering advanced data-based services, including database management and analytics to insurers & bankers.

AI and machine learning in a GDPR environment.

GDPR refers to the EU’s upcoming data protection regime. Find out whether the anonymisation of data, as prescribed by GDPR, would break AI models and more here.

Cultural diversity drives better AI outcomes

Agile organisations that can respond to the global challenges of their often multinational customer base are often the ones that thrive. Read more in this guide.

Why cant lending be like Uber?

Lending is constantly changing with entrants, regulations and technology. Learn how technology can give businesses market leading edge like Uber in this guide.

Why are Insurers playing a guessing game?

Numerous insurers overlook advanced solutions. Make sure your company leverages valuable insights from its data to enhance the user experience with Optalitix!

The future of life insurance

In the past, choosing the right life insurance was an arduous task. Thanks to data analysis and algorithms, shopping for life insurance has become much simpler.

Insurance quote personalisation is magic!

Dani Katz talks about how Optalitix can improve every aspect of the insurance business through better use of data, quotations and more. Read more in this guide.

A meaningful connection. The next phase of API relationships.

Data analytics and API closely intertwine, but what is the next phase in their relationship? Learn more about this successful financial connection here.